Your payment history is the largest component of your credit score. It basically looks at whether you’ve kept up to date with all your payments.

It answers questions in your prospective lender’s mind like, can I trust this borrower to pay me on time, let alone pay me at all?

Delayed payments appear in our credit reports and are known as late payments.

For some of us, late payments might have accumulated on our report from a different life. Maybe we missed a couple of payments because we were made redundant or were facing a emergency which required all our finances. As of late though, our financial situation has improved and our payments are back on track.

Surely those old late payments shouldn’t affect our chances of getting new credit, right?

The sad truth is, even though we ended up paying off the account in full, late payments still remain on our credit reports for up to 7 years. Having black marks like those can crush our chances of getting a new loan or raise our interest rates to sky high levels.

It’s not all doom and gloom, however. There’s a plethora of success stories of people getting late payments wiped from their record. Now, it’s time for you to be one of them.

Today I’m going to show you a step-by-step way to identify, prioritize and remove late/missed payments from your credit report. It’s going to be a long guide, but the payoff will be invaluable if you’re successful in wiping late payments off your report.

Step 1: Get your credit report

An important first step is to get your credit report ASAP. Your credit report contains a record of all your delinquent payments.

This will allow you to take stock of how your payment history looks.

Just picture what a lender might think when they look at your credit report. In their eyes, it’s simple:

If you were good with your debt repayments before, you’re likely to be good with them again in the future.

That’s why it’s imperative that you knock off any late payments from your credit report that might affect their image of you as a responsible borrower.

If you’re looking for free credit scores and credit reports, you can look at ClearScore for the UK and Experian for the US. What I really like about these providers is that not only can you get a comprehensive report for free, but you can also get it regularly. Regular monitoring is crucial for when you’re making improvements to your credit report.

Step 2: Identify past due accounts

With your credit report in hand, go through and identify any late payments.

You can tell if an account has late payments by looking for the words “past due”. In some credit reports, delinquent accounts can be found under the heading “potentially negative items”.

I’ve circled some examples from sample Experian reports:

Source: Experian

Source: Experian

Now, record down every late payment you can find.

If you’re lucky, you’ll find a single offending late payment account that you can focus on. If you’re like the rest of us though, you might have chalked up a number late payments.

You might even have some bills and loan repayments left outstanding.

Yikes.

How do you decide which one to tackle first?

Step 3: Prioritize where you need to take action

Before you get overwhelmed by the mountain of missed payments that await you, understand this crucial point:

Not every late/missed payment is weighted equally.

So here’s the trick – you should prioritize managing accounts that will get you more bang for your buck. Essentially, you want the most impact for the least amount of work.

How do you figure out which account has most impact/least work?

The one you address first should meet the following five (5) criteria:

- Most recent: How recent were the late payments?

- Least frequent: Which account has the least late payments?

- Most severe: Which late payments were the most days overdue?

- Highest interest: If unpaid, which account costs me the most if left unaddressed?

- Most relevant: What type of account is my prospective lender most likely to be interested in?

I’ll elaborate more about each criteria in turn.

1. How recent were the late payments?

Here’s a principle that applies generally in the world of credit scores:

If you want high impact improvements, address recent stuff first.

Now, it’s widely accepted that lenders place more emphasis on recent payments.

Why?

Lenders are far more concerned with your ability to pay now.

For example, you may have demonstrated that you were financially responsible by diligently repaying your loan which closed 5 years ago. However, if you’ve been missing payments recently, or worse, still have outstanding balances; then a lender might infer that you’ve run into financial difficulties.

Summary: Even if you used to be good at paying but now you suck = bad for the lender.

Credit reference agencies recognize this fact too, and calculate your credit score by weighting your recent financial behavior more heavily.

That’s why removing recent late payments first can have the greatest impact on your credit score.

As a side note, your recent credit activity stays on your credit report for longer vs. a late payment that might drop off your report in a year. So you can make more progress by clearing recent late payments from your credit report.

2. Which account has the fewest missed payments?

Imagine if you had history of countless on-time payments month after month. But then maybe there was one month where finances were tight, or you simply forgot to pay. Now you’ve got late payments in your payment history.

Kinda like this guy:

Don’t worry. When you have very few missed payments, it is far easier to convince a creditor to erase them. Of course, this is assuming that your account is current.

If you can point to an established history of prompt payments, it will indicate a strong relationship with your creditor and your good intentions to pay. They might be more willing to erase late payments because hey, that’s what friends are for.

They are also more likely to be convinced that you missed payments by mistake if you have this great repayment history.

Therefore, focus on accounts with the least number of late payments because it will be much easier to get them taken off.

3. Which late payments are the most days overdue?

How severe a late payment is, depends on how many days it is overdue (and also the amount that’s overdue.)

A payment that was 120 days overdue not only impacts your credit score more severely; it looks terrible on your credit report. From a prospective lender’s perspective, it will definitely raise doubts about how financially responsible you are.

Now compare that to a payment that was 30 days overdue. It’s far easier in this case to assume that the 30 days payment was merely an oversight.

So, try to get the long overdue payments off your credit report first, as it has a greater impact on your score and loan application success.

4. Which account carries the highest interest?

If your late payment is still due (meaning you have an outstanding balance with your creditor), then first settle the ones that carry the highest interest.

While I know that this doesn’t directly affect your payment history immediately, I wouldn’t be a friend if I didn’t tell you to prioritize paying off high interest loans first.

Not only do high interest loans bleed you dry with interest, but it is so hard to ever repay the principal when you’re doing minimum payments every month.

If left untouched, these loans snowball into massive utilized credit, which in turn negatively affects your credit score. So address them first.

5. Why are you trying to improve your credit score?

This is more of a bonus tip because it only applies to certain loan applications.

Why you’re improving your credit score can help you decide which accounts to tackle first. Are you aiming to get a car loan or apply for a new mobile contract? The purpose for improving your credit is important.

How come it’s important?

Different lenders place more weight on how you managed some loans more than others depending on which industry they’re in.

For example, car financiers are far more concerned with how well you’ve managed your auto loan. In fact they even use a special Auto Industry Option Score in assessing your credit risk. This auto enhanced score is derived from your usual credit score, but places greater emphasis on your auto loan repayments.

Apparently, auto lenders realized that people with poor credit histories still kept on top of their auto loans while letting their other credit accounts go into default. Use this to your advantage.

Yes, paying off all your accounts is important, but if you’re hoping to get a car loan in the future, focus on settling the account that is most relevant to your goals.

Now rank which late payments you’d like to remove first

For example, I put my loans into a spreadsheet and ranked each account for each of the criteria above. For each account, I added the ranks in each column together to get a total, as shown below:

As you can see, the auto loan got the lowest points, indicating that it ranked higher on each criteria (when taken together). Therefore, i focus on that account first.

Step 4: Take Action

Now that you’ve got an ordered list of accounts to address, it’s time to take action.

For each item that you’re looking to remove, one of two things could happen:

- The late payment is a blatant error, or

- You’re actually responsible for missing the payment.

Whether the late payment falls into one of these categories dictates what action you should take.

1. The late payment is a blatant error

You’re dead certain that you made prompt payments on your account, but your credit report shows you made a late payment. It can be infuriating for conscientious people to have their loan applications denied because of an error in their credit report.

Shockingly, it is not all that uncommon. Just have a gander at this hilarious yet sobering video from Last Week Tonight on credit report errors.

To correct an error, you need to first send a Dispute Letter along with identifying information, the items that you wish to dispute (circled on your credit report), and proof to support your argument (receipts, bank statements etc.) to the credit reporting agency.

The credit reference agency will then verify this with the creditor.

At the same time, you need to inform your creditor that you are disputing items in your credit report.

The credit dispute process can take anywhere from a few days to over a month. Some advocate dealing with the creditor directly to avoid the waiting time.

After it’s done with the investigation, the credit reporting agency will inform you in writing of the result, as well as furnishing you with an updated credit report.

If the error is found to be genuine, then your creditor should update all credit reporting agencies. However, you must still be proactive in checking that the error is truly corrected.

2. You’re responsible for the late payment

Yes, this may be less ideal than having a credit report error, but it’s not something that is beyond repair.

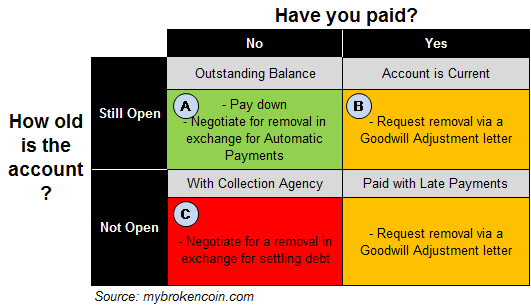

What you do to address these late payments depends on whether you’ve paid and whether the account is still open. I’ve summarized this in a decision matrix below:

I’ve color coded the types of late payments by how difficult I think they are to remove. Green is the easiest to manage and red is the most difficult. Let’s look at each in turn.

A. Your late payments relate to outstanding balances on an open account

This situation is where your account is open (meaning there are future payments to be made) and the payments that you’ve accumulated on that loan is overdue.

These facts tell me that your late payment is fairly recent and that your creditor is likely to be motivated to help you in your repayments (because you still owe them money.)

Assuming you are able and willing to pay, I suggest that you pay it off quickly. Do this first.

As we both know, this won’t get rid of the fact that you made a late payment. It would suck to have paid off this late payment not long after it was incurred and then have to wait 7 years for it to fall off your record.

That’s why you must negotiate with your creditor to expedite or remove the late payment. You can do this by writing in to your creditor and very politely:

- Explaining the reasons for late payment (whether you overlooked it, or you had a financial emergency etc.)

- Requesting that they expedite the process (because you’ve been so good with payments and are afraid that this one blemish will affect your chances of getting a mortgage etc.)

- Offering to sign up for automatic payments in order for the late payment to be removed.

- Emphasize that you wish to maintain good relations with the creditor.

B. You’ve paid what you owe and would like your late payments removed

This applies to both open and closed accounts where you have no outstanding balances on the account.

In this instance, you’ll want to ask for a Goodwill Adjustment from your creditor. Similar to the letter you’d write in point A, you should also explain your late payment and kindly request for the lending party to remove the late payment record.

If you’ve prioritized this account like we suggested above, it should have very few late payments. You can point this out to your creditor as a sign of a strong and positive relationship.

In addition, the fact that you’ve paid your account in full is also a positive signal to the lender and they are likely to view your proposition in a better light.

C. You have not paid what you owe on a collection account

This is where the amounts you owe have been overdue for a long period of time (typically 180 days.) Your lender has handed your account over to a collections agency which specializes in hounding you for repayment.

For you to get to this point, I’m guessing that you’ve deliberately let multiple payments go unpaid, whether it was because of financial difficulties or pure defiance. As such, any late payment is unlikely to be wiped from your credit report early.

Continue waiting out the loan

If you’re intent on not paying, waiting for the late payment to run its seven (7) year course is the likely the only way it will disappear from your credit report. Fortunately, the more time that elapses from when the account was passed to the collections agency, the less impact it will have on your credit score.

While waiting out the late payments is a possible option, it is not ideal. A collection account makes you look like a huge credit risk, and which of us really wants to be harassed by collections agencies for the next few years?

Settle the debt and request for removal

Sometimes, it is possible to negotiate with a lender to delete the collection account if you settle the debt. This is called pay to delete.

If you end up choosing to bring the outstanding balance to zero, you should strongly consider negotiating with the creditor to settle for less than the full balance (instead of paying in full.)

Some negotiating strategies include:

- Paying less than full balance if you make a lump sum payment up front

- Working out a repayment schedule, but over a longer period of time than originally intended

In effect, a settlement achieves the same result as paying the loan in full because the outstanding amount gets wiped from your record. The great difference is that you’ll be paying less than what you originally owed, or you’ll have a longer time to pay it.

Once you’ve settled the debt, you’ll be in a better position to request for your creditor expedite the removal of the delinquent record. You can read this inspiring story on how a person was able to convince his creditors that he was trying to rebuild his credit and that his delinquent payments were due to difficulties he faced after being diagnosed with cancer.

It’s definitely worth a shot. You really have to emphasize how your circumstances have changed and how you’re looking to rebuild your life. You could even point to your efforts to settle the debt instead of running away.

Do note that the seven years aging process will reset upon partial payment/correspondence with the collections agency. So be absolutely sure that you’re committed to settling the loan.

If your creditors refuse to erase your late payment history

While people have had success negotiating and convincing their lenders to wipe late payments off their credit report, not every creditor is as kind.

If you find that your creditor refuses to erase your late payment history, there are a couple of things left to do:

Letter of Explanation: This is similar to the other letters that we discussed earlier. However, this time, you’re addressing it to your prospective lender to whom you’re applying for a loan.

You need to explain why you were late with payments and emphasize how your circumstances have changed since then.

Notice a common thread between all the letters we’re writing? In each situation, you’re trying to show that you have a high current ability to pay, and your previous delinquencies are a poor reflection of that.

Notice of Correction: Okay, this only applies to consumers in the UK. Basically, credit referencing agencies in the UK will allow you to add a 200 word note to your credit report to explain the late payments. Again, you’re aiming to show how your circumstances have changed since your delinquency.

Rebuild Credit: It really sucks to have blemishes on your credit report. Kind of like a dark spot on clean linen – it may be small, but immediately noticeable.

However, it’s not the be all and end all. Payment history is merely a subset of your entire credit report, and your credit report is a subset of all the factors that go into a lender’s consideration in accepting you as a borrower.

There are numerous other factors that contribute to your credit score, such as the current amount of credit you’re utilizing and lines of credit open to you. You can work on these other areas to help improve your credit score.

Remember too that as your late payments age, they naturally carry less impact on your credit score. So, the important thing is to keep on top of your new payment obligations.

Conclusion

After you go through the long and arduous exercise of eliminating late payments and collection accounts from your report, you might be eager to see how much it improved your credit score.

It’s hard to tell you the exact number of points your score will improve by. This is because the impact of late payments vary depending on how old they are. However, there are some people who have found that their scores can immediately improve by about 20 points.

I think the more important point should be how your credit report (or financial CV) looks to a prospective lender.

This guide is not about “hacks” or gaming your credit score. You need to look at your credit the way a human being (your lender) will look at it. They want to see that you’re genuinely financially sound and responsible.

Reducing late payments is merely a byproduct of being financially savvy. Your credit score will naturally come to reflect that with time.

Focus on being financially savvy as your end goal. Being obsessed with your credit score itself is like losing the wood for the trees.

I hope that by reading this article, you’ve gained a roadmap to taking off late payments from your credit report. No improvements to your credit report are easy, but they’re definitely worth it.